June 8, 2026

QUICK ANSWER

Chemical company energy hedging is the practice of using financial instruments — swaps, options, caps, and collars — to stabilize the cost of natural gas, power, and gas-linked feedstocks that drive a chemical producer's margins. The goal is to protect budgeted margins from price spikes while preserving enough flexibility to benefit from lower input costs.

For most chemical manufacturers, energy and feedstock are the single largest controllable variable costs. Natural gas is both a fuel and, through ethane and other NGLs, a feedstock — so a move in the gas market hits the P&L twice. A hedging program that is designed around the actual exposure, rather than bolted on reactively, is what separates predictable margins from earnings surprises.

Why is energy such a large riskfor chemical producers?

- Dual exposure: natural gas fires the plant and, via ethane/propane, is the raw material for olefins and downstream products.

- Volatility: gas and power prices can move sharply on weather, storage, and geopolitics —the Gulf Coast is especially exposed during hurricane season.

- Thin, cyclical margins: competitors in regions with cheaper energy can undercut on price, so an unhedged cost spike is also a competitive risk.

Because the exposure is structural, the question is not whether to manage it but how to do so with discipline.

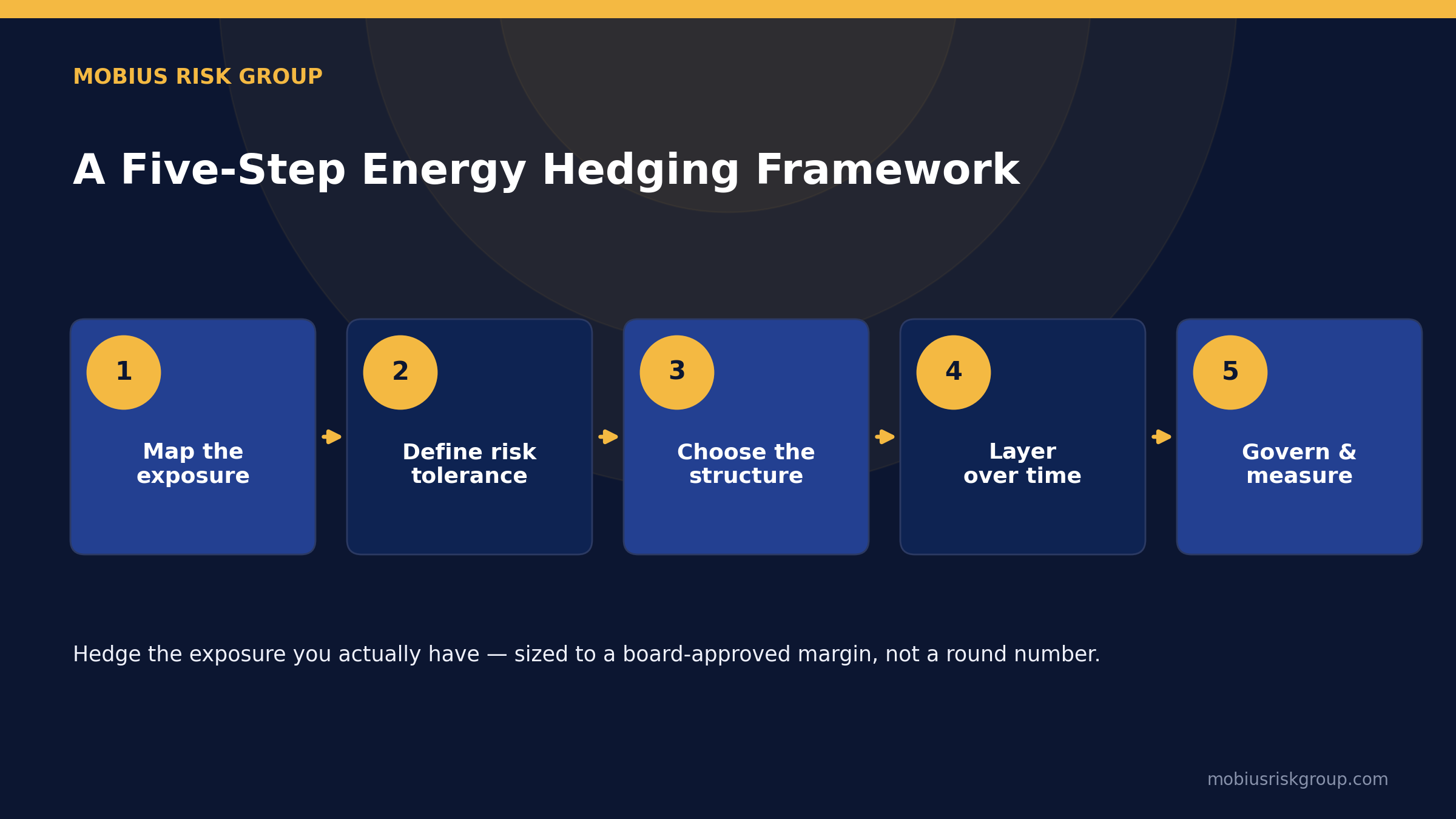

A five-step hedging framework for chemical CFOs

1. Map the exposure: Quantify how much gas, power, and NGL feedstock the business consumes, and translate it into a monthly volumetric exposure. Hedge the exposure you actually have — not a round number.

2. Define the risk tolerance: Decide what you are protecting: a board-approved Decide what you are protecting: a board-approvedmargin, a budget rate, or a covenant. The objective sets the instrument.

3. Choose the structure: Match instrument to goal — swaps to lock a rate, caps to Match instrument to goal — swaps to lock a rate, caps tolimit the upside of cost, collars to bound both sides at low or zero premium.

4. Layer over time: Hedge a rising percentage of near-term months and a smaller share of later months, so the program is never fully exposed and never fully Hedge a rising percentage of near-term months and a smallershare of later months, so the program is never fully exposed and never fullycommitted.

5. Govern and measure: Mark the portfolio to market, monitor effectiveness, and report against the original objective — ideally through an independent, unconflicted advisor and a single analytics platform.

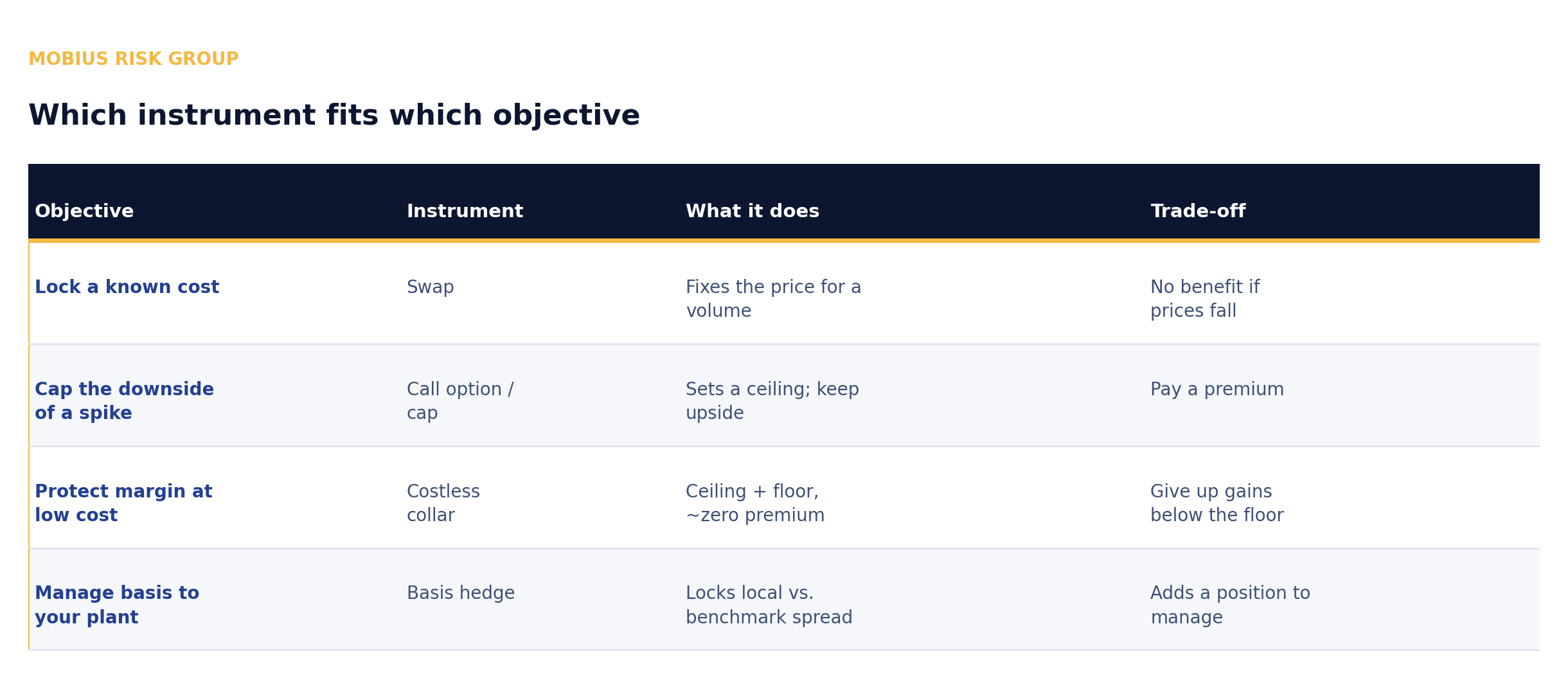

Which instruments fit which objective?

Each hedging objective points to a different instrument. The graphic below maps the four most common goals—locking a cost, capping a spike, protecting margin cheaply, and managing basis—to the structure that fits and the trade-off it entails.

The takeaway: swaps buy certainty at the cost of upside; caps buy protection for a premium; costless collars protect margin at little or no cost by giving up some upside; and basis hedges address local delivery risk rather than outright price.

A common mistake is defaulting to swaps for everything. Swaps remove volatility but also remove the benefit of falling prices — a poor fit when a producer wants protection against spikes but room to breathe if the market softens. That is where caps and collars earn their place.

How much should a chemical company hedge?

There is no universal ratio, but a layered approach is widely used: hedge a higher share of the next 6–12 months (when budgets are firm) and a declining share further out. This keeps the program responsive to new information and avoids locking in a single price for years. The right ratios follow from the margin objective set in step two, not from a market view.

Frequently Asked Questions

Why do chemical companies hedge energy?

Because natural gas and power are their highest variable cost and also feed into raw materials. Hedging stabilizes margins against price spikes, protects budgets and covenants, and reduces earnings volatility.

What is the best hedging instrument for a chemical producer?

It depends on the objective. Swaps lock in a fixed cost, caps limit downside from a price spike while preserving upside, and costless collars protect margin at little or no premium. Most programs blend instruments across time.

How much of its energy use should a chemical company hedge?

Typically, a layered program hedges a larger share of near-term months and a smaller share of later months. The exact ratio should be determined by a board-approved margin or budget objective rather than a market forecast.

Should a chemical company hedge through its bank?

A bank can execute hedges, earn the spread, and take the other side. Many producers use an independent, unconflicted advisor to design and oversee the program, and to ensure execution remains competitive.

Subscribe to receive the latest Mobius Research & updates