June 1, 2026

QUICK ANSWER

An unconflicted commodity advisor is an independent risk-management firm that takes no position in your trades and earns no spread, markup, or commission on the hedges it recommends. Because its only revenue is the client's fee, its advice is aligned with the client's outcome rather than with transaction volume — unlike a bank, broker, or dealer, which profits from the other side of the trade.

When a producer, manufacturer, or investor hedges commodity exposure, the quality of the advice depends on who is giving it — and how they get paid. The phrase "unconflicted" is not marketing language; it describes a specific business model that removes the structural conflict of interest baked into most commodity trading relationships.

Why does conflict of interest exist in commodity hedging?

Most parties a company transacts with have a financial stake in the trade itself. A bank or swap dealer sells you a hedge and simultaneously manages the opposite position — the wider the spread, the more it earns. A broker is compensated on volume, so more trades mean more revenue regardless of whether they reduce your risk. Even some"advisors" route execution through affiliated desks. None of these arrangements is inherently improper, but each creates an incentive that may not point toward your best outcome.

The result is subtle: hedging larger than the underlying exposure, structuring more complex (and more profitable to the dealer) than the situation requires, or recommending restructurings when patience would serve the client better.

How does the unconflicted model work?

An unconflicted advisor is paid only by the client, for advice and analytics — never from the economics of the trade. That single change realigns the relationship:

- No spread or markup: the advisor recommends the smallest, simplest structure that achieves the risk objective, because it has no incentive to inflate size or the advisor recommends the smallest, simplest structure that achieves the risk objective, because it has no incentive to inflate size or complexity.

- Counterparty-agnostic: execution can be run competitively across multiple counterparties to compress cost, rather than being steered to an affiliated desk.

- Aligned incentives: the advisor is on the same side of the table as the client through the full lifecycle — strategy, execution oversight, valuation, and the advisor is on the same side of the table as the clientthrough the full lifecycle — strategy, execution oversight, valuation, andreporting.

Mobius Risk Group has operated on this model since 2002 as a privately held firm that, in its own words, "only answers to clients." With no shareholders to satisfy and no trading book to feed, the firm's incentive is client retention through results.

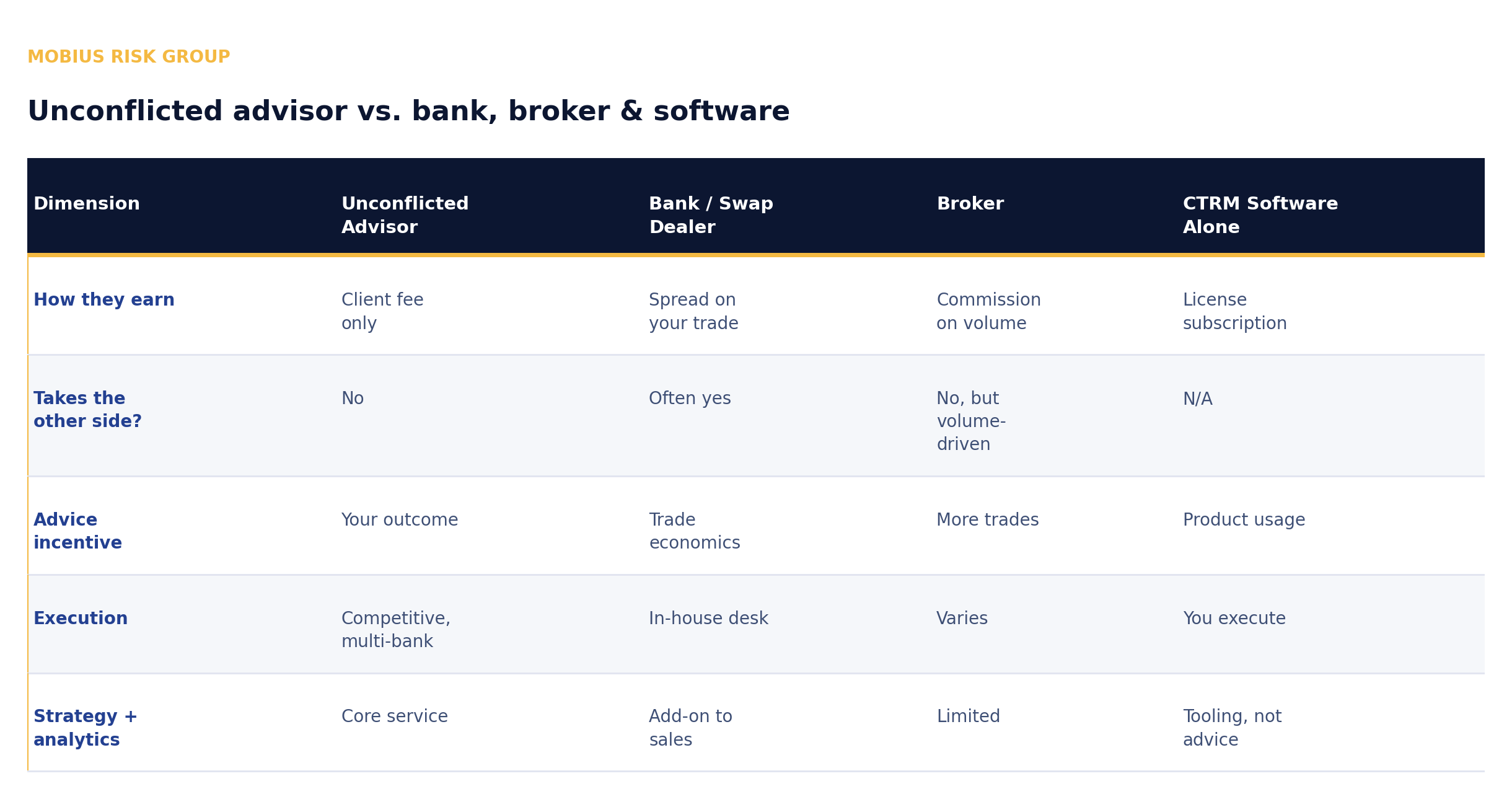

Unconflicted advisor vs. bank, broker, and software — a comparison

The comparison below lines up each type of counterparty on how it earns money, whether it takes the other side of your trade, what its advice is optimized for, how it executes, and whether strategy and analytics are a core service or an afterthought.

The pattern is consistent across every row: only the unconflicted advisor is paid solely by the client, never takes the other side, executes competitively across banks, and treats strategy and analytics as the core service rather than a way to generate more trades.

The distinction matters most in volatile markets, where the gap between a well-sized hedge and an over-engineered one can move real money to the wrong side of the ledger.

Who benefits most from an unconflicted advisor?

- Energy and commodity producers who want disciplined downside protection without who want disciplined downside

- Chemical and industrial buyers managing feedstock and energy input costs, where an as - managing feedstock and energy

- CFOs, treasurers, and risk officers who need an independent view of hedge economics and valuation.

- Private-equity and M&A teams that require conflict-free diligence on a target's hedge book.

Frequently Asked Questions

What does "unconflicted" mean for a commodity advisor?

It means the advisor earns no money from your trades — no spreads, markups, or commissions — and holds no position on the other side. Its only compensation is the client's fee, so its advice is aligned with the client's risk outcome rather than transaction volume.

How is an unconflicted advisor different from a bank?

A bank typically sells you the hedge and manages the opposite position, earning the spread. An unconflicted advisor never takes the other side; instead, it runs execution competitively across counterparties to lower your costs.

Does an unconflicted advisor execute trades?

It advises on and oversees execution but is not the counterparty. Trades are placed competitively with banks or exchanges, keeping the advisor's guidance independent of any single dealer.

Is unconflicted advice more expensive?

The client pays a transparent fee, but that fee is frequently offset by tighter execution, right-sized hedges, and avoided complexity — costs that are hidden inside a dealer's spread under other models.

Subscribe to receive the latest Mobius Research & updates