May 11, 2026

QUICK ANSWER

For a CFO, commodity hedging is a finance decision, not a market bet. Its job is to protect budgeted margin, cash flow, and covenants from price swings using a written policy that defines objectives, approved instruments, coverage limits, and authority. Success is measured against that objective — not against where prices end up.

When commodity prices are a material input or revenue driver, they belong on the CFO’s desk. Hedging is how finance converts an unpredictable market into a planning assumption it can stand behind — protecting the budget, the covenant, and the earnings guidance. Done well, it is a governance discipline, not a trading activity.

Why is commodity hedging a CFO responsibility?

Commodity moves flow straight through to margin, cash flow, and covenant headroom — the numbers the CFO is accountable for. Left unmanaged, a price swing can blow a budget, breach a covenant, or force a guidance revision. The CFO’s role is not to predict the market but to decide how much of that uncertainty the business should carry, and to put controls around the rest.

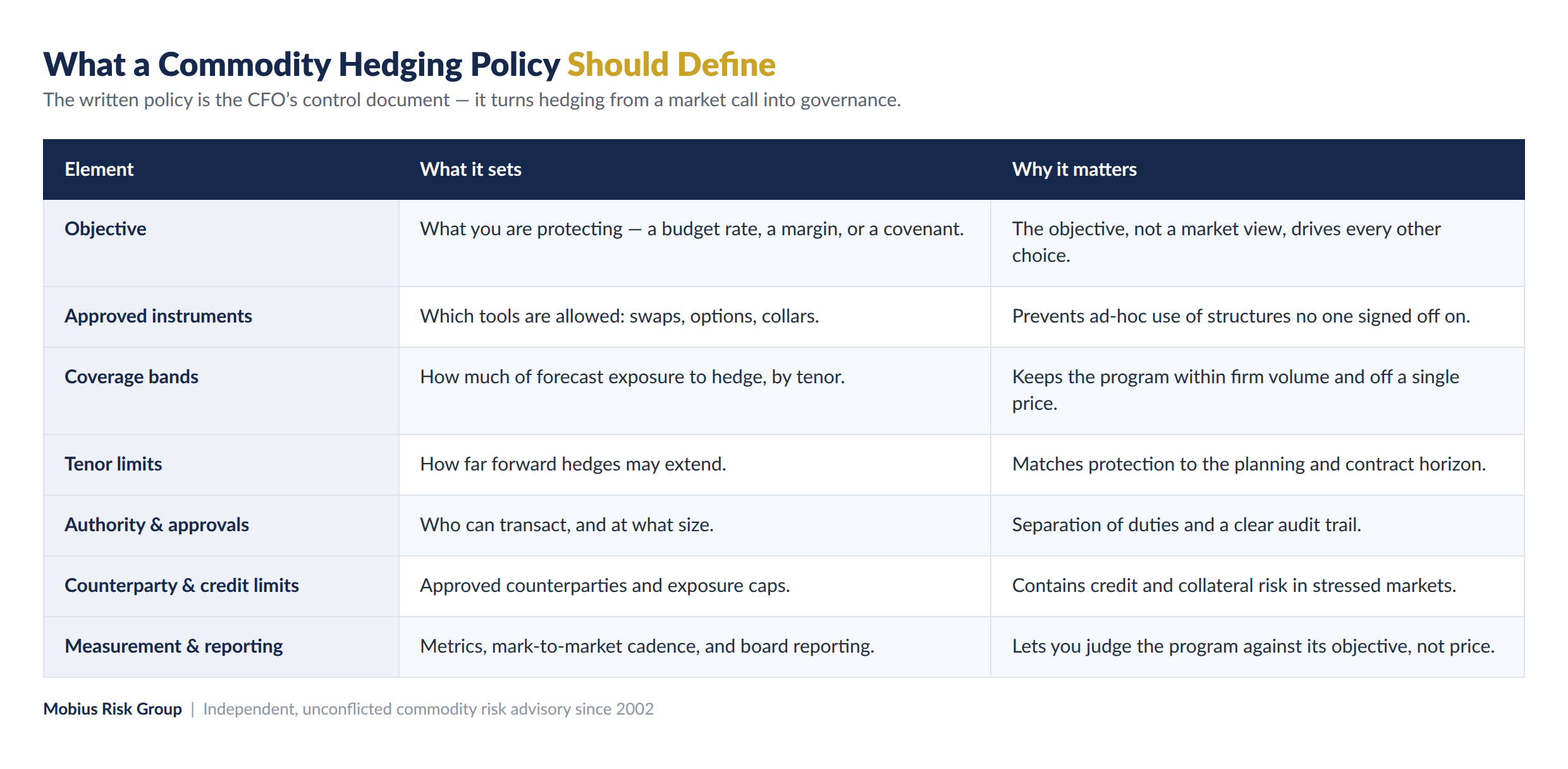

What should a commodity hedging policy contain?

The written policy is the CFO’s control document. It turns hedging from a series of ad-hoc calls into a governed program with clear objectives and limits. The table below lists what a complete policy defines.

The most important line is the first one: the objective. Whether you are protecting a budget rate, a margin, or a covenant determines the instrument, the coverage, and how you measure success. Everything else in the policy follows from it.

How should a CFO measure whether hedging is working?

The test is not whether a hedge “made money” — a hedge that loses value while the underlying exposure gains is doing its job. Measure the program against its objective: Did budgeted margin hold within the target range? Did cash flow stay above the covenant threshold? Was realized price within the intended band? Judging hedges on standalone P&L invites exactly the wrong behavior, because it rewards taking a view rather than reducing risk.

What about hedge accounting and covenant compliance?

Two finance-specific considerations sit alongside the economics. Hedge accounting can reduce earnings volatility by matching the timing of hedge gains and losses to the underlying exposure, but it carries documentation and effectiveness-testing requirements that should be scoped early. [confirm applicable accounting standard and treatment] Separately, lender agreements often mandate minimum hedge levels or restrict certain structures — so the policy must be written to satisfy covenants, not just market objectives.

How does a CFO govern and report on the program?

Governance is what keeps a hedging program defensible. Clear separation of duties between who decides, who transacts, and who reports; approved counterparty and credit limits; a regular mark-to-market and exposure report to the board or risk committee; and periodic review of the policy itself. The goal is that anyone — an auditor, a lender, a board member — can see why each position exists and how it maps to the stated objective.

Where does an unconflicted advisor fit?

Many finance teams do not have a dedicated commodity desk, and the parties offering to help are often the same banks that earn the spread on the trade. An unconflicted advisor — paid only by the client, with no trading book — helps write the policy, benchmark pricing, and report on the program without a stake in how much you transact. Mobius Risk Group provides exactly this: policy and strategy support, exposure and mark-to-market tracking in its RiskNet™ CTRM platform, scenario analysis via M(β)risk™, and independent benchmarking through M-Direct indicative pricing.

Frequently Asked Questions

Is commodity hedging a treasury or an operations function?

Both contribute, but the objective and the policy sit with finance. Operations informs the exposure forecast; the CFO or treasurer owns the objective, the limits, and the reporting.

How do you measure hedging success?

Against the objective, not standalone P&L. If the goal was to protect a budget rate or covenant and it held, the program worked — even if an individual hedge lost value while prices moved favorably.

Does a company need a written hedging policy?

Yes. A written policy defines objectives, approved instruments, coverage and tenor limits, authority, and reporting. It provides governance, an audit trail, and often satisfies lender and board requirements.

Should a CFO hedge through the company’s bank?

A bank can execute hedges but also earns the spread and may take the other side. Many finance teams use an independent, unconflicted advisor to design and oversee the program and keep execution competitive.

Subscribe to receive the latest Mobius Research & updates