March 30, 2026

QUICK ANSWER

A deal-contingent hedge is a hedge that only becomes effective if a transaction closes. It lets an acquirer or financing party lock in commodity (or rate or FX) economics during the gap between signing and closing — and if the deal falls through, the hedge simply never activates, so there is no unwanted position to unwind. The protection carries a premium for that contingency.

Between signing and closing, an energy deal is exposed: prices can move for weeks or months while regulatory approval and financing complete, eroding the economics that justified the price. A deal-contingent hedge closes that gap without creating a new risk if the deal does not happen.

How does a deal-contingent hedge work?

The hedge is written so it activates only on close. If the transaction completes, the buyer has locked the price it modeled; if it does not, the hedge disappears with no settlement obligation. That contingency is the whole value — and the reason it costs more than a standard hedge.

How is it different from a standard hedge?

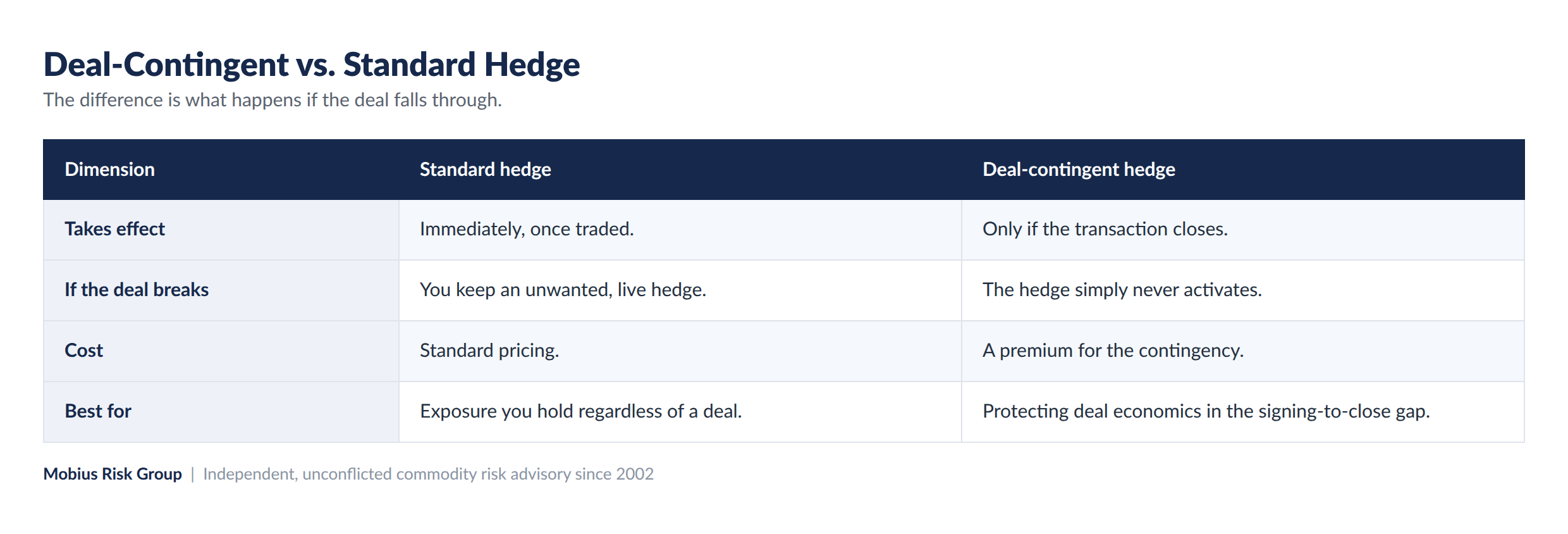

The difference shows up entirely in the “what if the deal breaks” scenario, as the table makes clear.

With a standard hedge, a failed deal leaves the buyer holding a live position it never wanted. With a deal-contingent hedge, that risk is removed — which is exactly why it is used in M&A and financing.

When should you use one?

Deal-contingent structures fit situations where a buyer wants to protect the economics of a specific transaction but cannot risk carrying a hedge if the deal collapses — acquisitions, project financings, and similar. They require modeling the combined, post-close exposure rather than the target’s book alone.

How Mobius Risk Group helps

Mobius provides independent, unconflicted support on deal-contingent and bridge hedges — modeling exposure, structuring the hedge, and benchmarking pricing — without earning a spread on the trade.

Frequently Asked Questions

What is a deal-contingent hedge?

A hedge that only takes effect if a transaction closes, letting a buyer lock deal economics during the signing-to-close period with no position to unwind if the deal breaks.

Why does a deal-contingent hedge cost more?

Because the counterparty bears the risk that the deal fails and the hedge never activates. That contingency is priced as a premium.

When are deal-contingent hedges used?

In M&A and project financing, to protect commodity, rate, or FX economics between signing and closing without risk if the transaction does not complete.

Subscribe to receive the latest Mobius Research & updates