June 29, 2026

QUICK ANSWER

In energy M&A, commodity price risk drives both what a target is worth and whether that value survives to close. It shows up in the price deck behind the valuation, the target’s existing hedge book and its mark-to-market, the price gap between signing and closing, and lender hedge covenants. Managing it means diligencing the hedge book independently and protecting value through the deal, not just modeling it once.

Energy assets are, at their core, leveraged bets on commodity prices. That makes commodity price risk one of the largest and most underestimated variables in an energy acquisition: it can swing enterprise value, distort a target’s reported performance, and quietly transfer value between buyer and seller in the weeks between agreement and completion.

Why does commodity price risk drive energy deal value?

An energy target’s cash flows rise and fall with the forward curve, so the price deck used in the model is one of the biggest levers on valuation. Two buyers using different curves — or different basis assumptions — can arrive at materially different enterprise values for the same asset. Before negotiating, a buyer needs an independent view of how sensitive value is to the curve, to basis, and to volatility, rather than accepting the seller’s deck at face value.

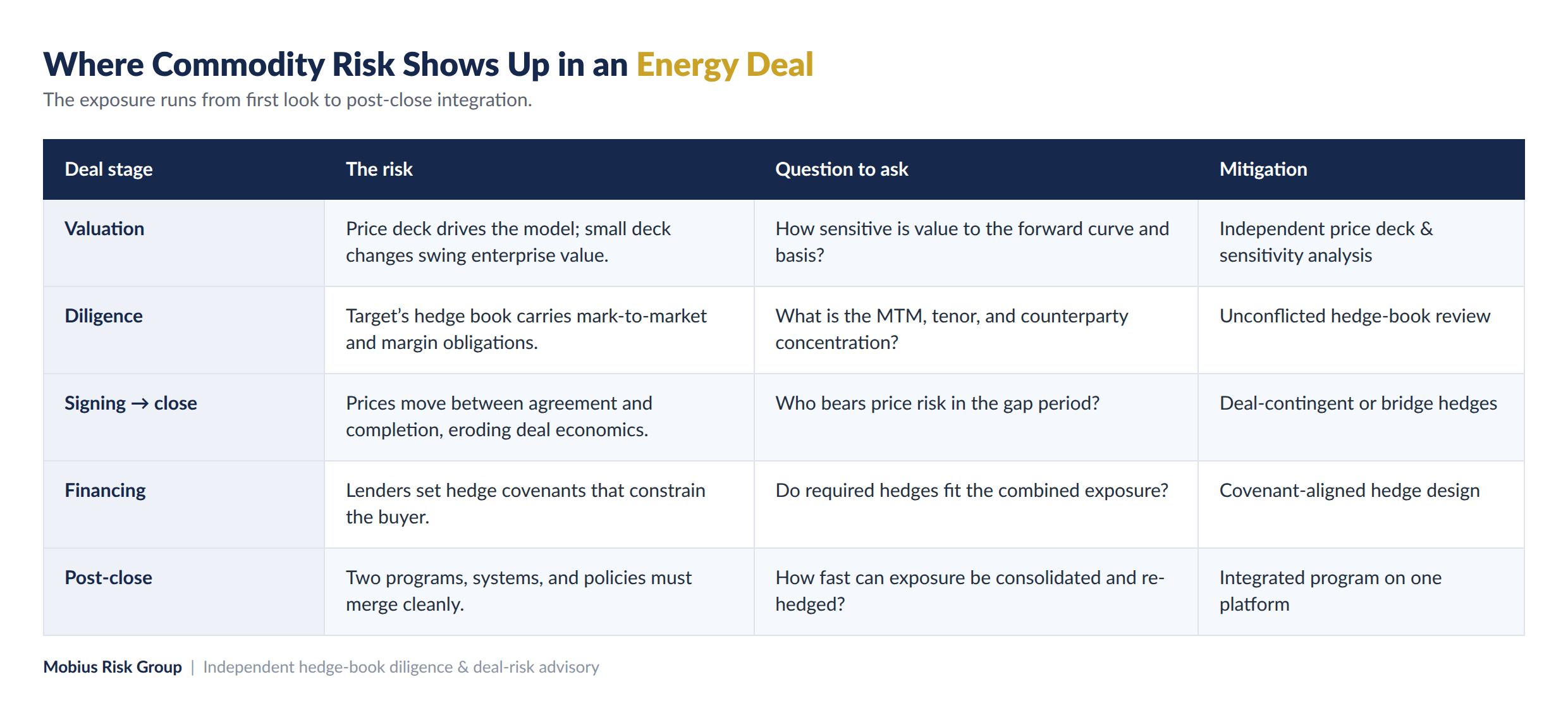

Where does commodity risk show up across a deal?

The exposure is not confined to the model; it runs from first look through integration. The table below maps where it appears and how to address it at each stage.

The pattern is that commodity risk is a thread through the entire transaction, not a single diligence checkbox — and the places it does the most damage (the hedge book and the signing-to-close gap) are the ones most easily overlooked.

How do you diligence a target’s hedge book?

A target’s existing derivatives portfolio can be an asset or a liability, and it is rarely neutral. Effective diligence establishes the current mark-to-market, the tenor and volume profile, counterparty and credit concentration, any margin or collateral obligations, and whether the hedges actually match the underlying exposure or introduce new risk. Because a bank or dealer that helped put those hedges on has an interest in how they are characterized, an unconflicted review — one with no stake in the positions — gives the buyer a cleaner read.

How do you protect deal value between signing and close?

Commodity prices do not pause while a deal works through regulatory approval and financing. If prices move against the buyer in that window, the economics that justified the price can erode before day one. Deal-contingent hedges — which only take effect if the transaction closes — and other bridge structures let a buyer lock the economics of the deal without taking on price risk if it falls through. Getting these right requires modeling the combined exposure, not just the target’s standalone book.

What happens to hedging after the deal closes?

At close, the buyer inherits two exposures, possibly two hedging policies, and often two systems. The faster the combined exposure can be consolidated, re-measured, and re-hedged to a single policy on one platform, the sooner the acquirer controls its risk. This is where an integrated CTRM platform and a clear post-close hedging plan turn a pile of inherited positions into a managed program.

How Mobius Risk Group supports energy transactions

Mobius Risk Group provides independent, unconflicted deal-risk advisory across the transaction lifecycle: independent price decks and sensitivity analysis for valuation, hedge-book diligence with no stake in the positions, structuring support for deal-contingent and bridge hedges, and post-close consolidation onto its RiskNet™ CTRM platform with M(β)risk™ analytics. Because the firm earns no spread or commission on the hedges involved, its read on a target’s book is not colored by who arranged it.

Frequently Asked Questions

Why is commodity price risk important in energy M&A?

Because an energy asset’s value is driven by commodity prices. The price deck shapes valuation, the target’s hedge book carries real gains or obligations, and price moves between signing and close can erode the economics that justified the deal.

What is a deal-contingent hedge?

A hedge that only becomes effective if the transaction closes. It lets a buyer lock in the deal’s commodity economics during the signing-to-close period without being exposed to price risk if the deal does not complete.

Should the target’s hedge book be reviewed in diligence?

Yes. The hedge book’s mark-to-market, tenor, counterparty concentration, and collateral terms can materially change deal value. An independent, unconflicted review avoids relying on the party that arranged the hedges.

Who should review commodity risk in a transaction — a bank or an independent advisor?

A bank can execute hedges but may also be a counterparty to them. An unconflicted advisor reviews the exposure and hedge book with no stake in the positions, giving the buyer an independent view of deal risk.

Subscribe to receive the latest Mobius Research & updates