May 4, 2026

QUICK ANSWER

Oil and gas producers hedge to protect cash flow, capital budgets, and lender covenants from price declines. Common tools are swaps (lock a price), collars (bound a range), three-way collars (cheaper protection with a gap on the downside), and puts (insurance with upside). The best programs size hedges to value at risk and to firm, developed production — not just to raw volume.

For an upstream producer, commodity price is the single biggest driver of cash flow and, therefore, of the capital budget. A hedging program is how a producer protects the drilling plan and the balance sheet from a downturn it cannot control — and, increasingly, how it satisfies the lenders funding its development.

Why do oil and gas producers hedge?

Three reasons dominate: protecting the cash flow that funds capital spending, meeting lender hedge requirements on reserve-based loans, and reducing the risk that a price drop forces a mid-year cut to the drilling program. Hedging does not raise the ceiling on a producer’s outcomes so much as it raises the floor — keeping the business funded and covenant-compliant through the low points of the cycle.

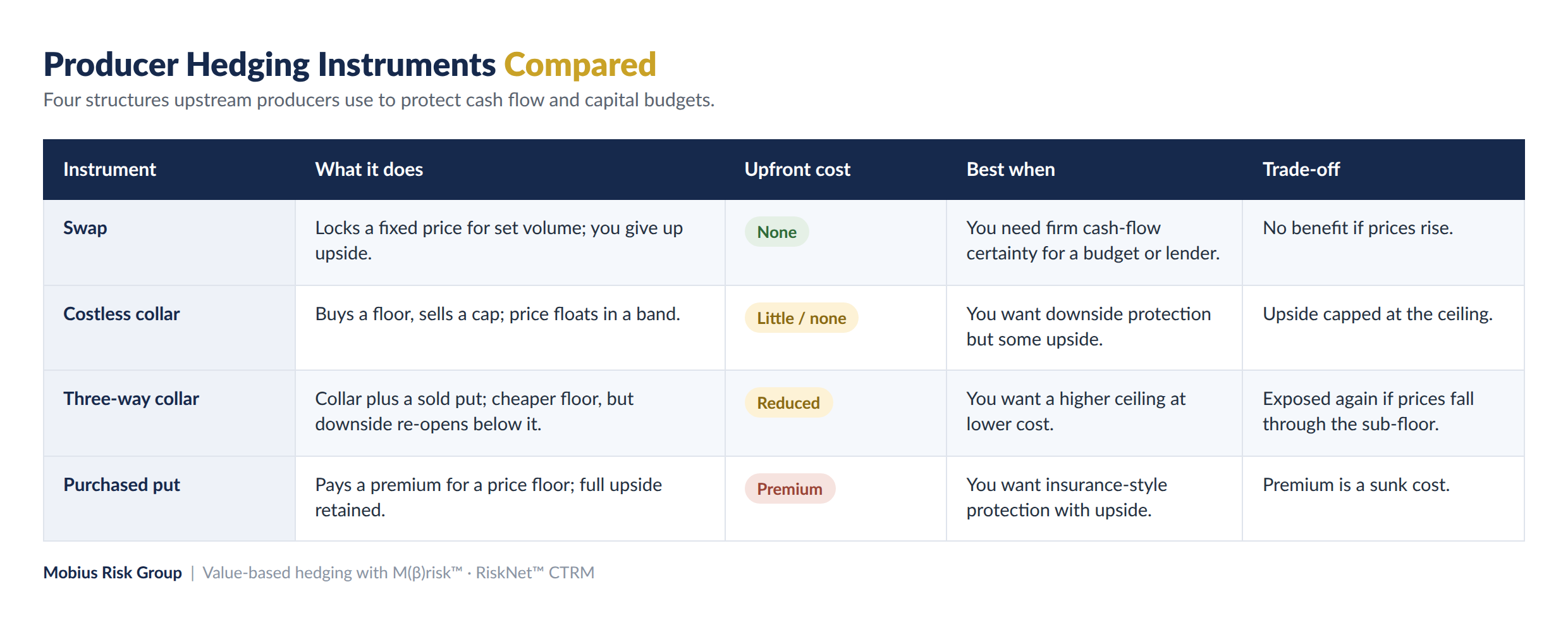

What are the main producer hedging instruments?

Producers assemble programs from a handful of building blocks, each with a different cost and protection profile. The table below compares the four most common.

Swaps give the firmest protection but surrender all upside; collars keep some upside for a capped ceiling; three-way collars lower the cost of that protection but re-open downside below a sub-floor; and purchased puts behave like insurance, preserving upside for an upfront premium. Most producers blend these across time and price levels rather than relying on one.

How much production should a producer hedge?

Coverage should track the certainty of the barrels and the demands on cash flow. Producers typically hedge a higher share of proved, developed, producing (PDP) volumes — the most certain barrels — and less of undeveloped or growth volumes. Lender requirements often set a floor on coverage for the near term. The guardrail is to avoid hedging more than firm expected production, which would turn a hedge into a speculative short.

Volumetric vs. value-based hedging: what is the difference?

Traditional programs hedge by volume — a set percentage of barrels or Mcf. Value-based hedging instead sizes protection to the risk to cash flow and capital plans, recognizing that not all volumes carry equal risk: NGL and crude exposure can be more volatile than gas, and location (basis) changes the picture. Mobius Risk Group built its M(β)risk™ analytics specifically to price this market-based deal risk, so a producer can hedge where the risk actually is rather than defaulting to a flat volumetric ratio. [confirm methodology naming]

How do lender hedge covenants shape a producer’s program?

Reserve-based lenders frequently require borrowers to hedge a minimum percentage of PDP production over a set horizon, and may restrict certain structures. These covenants protect the lender’s collateral value, but they can conflict with a producer’s own view or over-hedge less-certain volumes. Designing the program to satisfy the covenant while still fitting the true exposure is a core part of the work — and a place where independent advice helps.

What role does basis play for producers?

A producer sells at a local delivery point, not at Henry Hub or WTI. Regional basis — Waha, Midland, and others — can be large and volatile, so a benchmark hedge can leave a producer exposed to the spread between the benchmark and the wellhead. A complete producer program hedges basis alongside flat price rather than assuming the benchmark hedge covers realized revenue.

How Mobius Risk Group supports producers

Mobius Risk Group is an independent, unconflicted advisor that has worked with energy producers since 2002. It sizes and stress-tests programs with M(β)risk™ value-based analytics, tracks physical and financial positions in the RiskNet™ CTRM platform, benchmarks counterparty quotes with M-Direct indicative pricing, and helps producers design programs that satisfy lender covenants — all without earning a spread or commission on the hedges themselves.

Frequently Asked Questions

Why do oil and gas producers hedge?

To protect the cash flow that funds capital spending, to meet lender hedge covenants, and to keep the drilling program on track through price downturns. Hedging raises the floor on outcomes rather than the ceiling.

What is a three-way collar?

A collar (bought floor, sold ceiling) plus an additional sold put below the floor. It lowers the cost or raises the ceiling versus a standard collar, but re-exposes the producer to prices if they fall below the sub-floor.

How much of its production should a producer hedge?

Typically a higher share of proved developed producing volumes and less of growth volumes, within firm expected production and any lender minimums. The exact level should follow from cash-flow risk, not a market view.

What is value-based hedging?

Sizing hedges to the risk each volume poses to cash flow and capital plans, rather than to a flat percentage of volume. It accounts for differing volatility across products and for basis, so protection is placed where the risk actually is.

Subscribe to receive the latest Mobius Research & updates