June 15, 2026

QUICK ANSWER

To choose an unconflicted commodity risk advisor, verify four things: it is paid only by fees (no spreads or commissions), it never takes the other side of your trade, it stays instrument-neutral, and it can show independent pricing and analytics. Any “advisor” that earns more when you transact is not truly unconflicted.

Choosing a commodity risk advisor is really a question about incentives. Two firms can offer the same hedging advice, but if one profits from the trade and the other does not, the advice will drift in different directions over time. This checklist covers what to verify — and the red flags that reveal a sales desk wearing an advisory label. (For a primer on the model itself, see what an unconflicted commodity advisor is.)

What makes a commodity risk advisor “unconflicted”?

An advisor is unconflicted when it does not profit from the transactions it recommends: no trading book, no position opposite the client, and no commission or bid-ask spread on executed hedges. Its only revenue is the client’s fee, so its advice is aligned with the client’s risk outcome rather than transaction volume. Everything in the checklist below is a way of testing whether that is actually true.

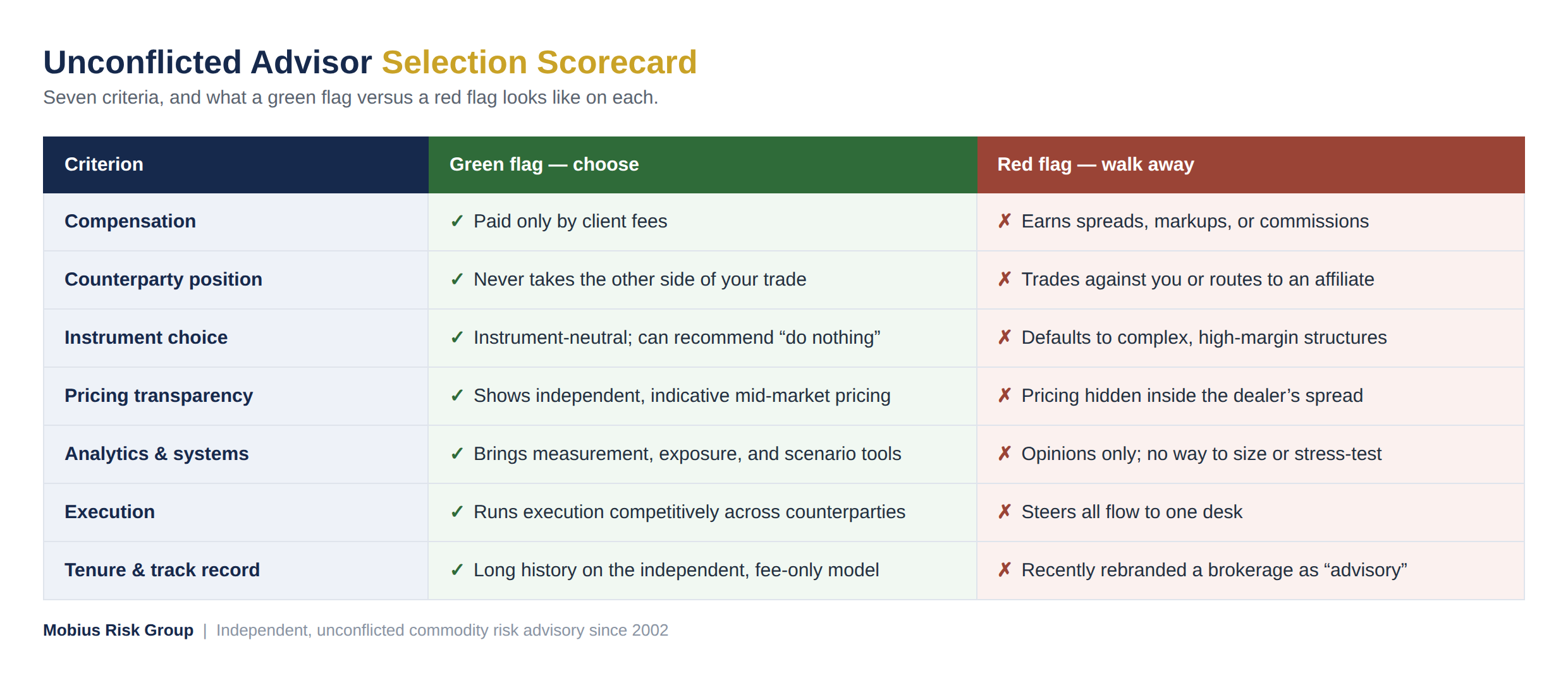

The 7-point checklist for choosing an unconflicted advisor

Score any prospective advisor against these seven criteria. The graphic below shows what a green flag versus a red flag looks like on each.

- Compensation — is the advisor paid only by client fees, or does it earn spreads, markups, or commissions on the trades it recommends?

- Counterparty position — does it ever take the other side of your hedge, directly or through an affiliate?

- Instrument choice — can it recommend a simple swap, or even “do nothing,” as readily as a complex structure?

- Pricing transparency — can it show you independent, indicative mid-market pricing so you can check counterparty quotes?

- Analytics & systems — does it bring measurement, exposure, and scenario tools, or only opinions?

- Execution — does it run execution competitively across counterparties, or steer all flow to one desk?

- Tenure & track record — how long has it operated the independent, fee-only model, and across which commodities?

How do you verify an advisor is really independent?

Do not take “independent” at face value — ask direct questions and listen for specific answers:

- “How exactly are you compensated on this engagement, and does that change if we trade more?”

- “Do you, or any affiliate, ever act as counterparty to our hedges?”

- “Can you show us indicative mid-market pricing before we take a dealer quote?”

- “Will you put in writing that you earn no spread, markup, or commission on our trades?”

A truly unconflicted advisor answers each of these plainly and is willing to document it. Hesitation is itself a data point.

What are the red flags of a conflicted advisor?

- Fee opacity — compensation that is bundled into the trade rather than billed transparently.

- Complexity bias — a standing preference for structures that happen to carry wider spreads.

- Single-desk execution — every trade routed to the same counterparty or affiliate.

- Volume nudges — frequent restructuring recommendations when patience would serve you better.

- Rebranded brokerage — a firm that recently relabeled a commission business as “advisory.”

How should an unconflicted advisor be paid?

Through a transparent advisory or retainer fee agreed with the client — not through spreads on hedges or commissions on trades. That fee is frequently offset by tighter execution, right-sized hedges, and avoided complexity, costs that are otherwise hidden inside a dealer’s spread.

How does Mobius Risk Group meet the checklist?

Mobius Risk Group was founded in 2002 in Houston and has operated the unconflicted, fee-only model since. It holds no trading book and earns no spread or commission on client hedges; it sits on the same side of the table as the client through strategy, execution oversight, and monitoring. The work is backed by RiskNet™ (CTRM) for exposure and position tracking, M(β)risk™ analytics for sizing and stress-testing, and M-Direct indicative pricing so clients can benchmark every counterparty quote independently.

Frequently Asked Questions

How do I know if a commodity risk advisor is truly unconflicted?

Confirm it is paid only by client fees, never acts as counterparty to your trades, and will document that it earns no spread or commission. If compensation rises when you transact more, it is not unconflicted.

What questions should I ask before hiring a hedging advisor?

Ask how it is compensated, whether it or an affiliate ever takes the other side of your trade, whether it can show independent pricing, and how long it has run the fee-only model.

Is an unconflicted advisor more expensive than using a bank?

You pay a transparent fee, but it is frequently offset by tighter execution, right-sized hedges, and avoided complexity — costs that are otherwise hidden inside a dealer’s spread.

Can an unconflicted advisor still execute my hedges?

It advises on and oversees execution but is not the counterparty. Trades are placed competitively with banks or exchanges, keeping the advice independent of any single dealer.

Subscribe to receive the latest Mobius Research & updates