March 23, 2026

QUICK ANSWER

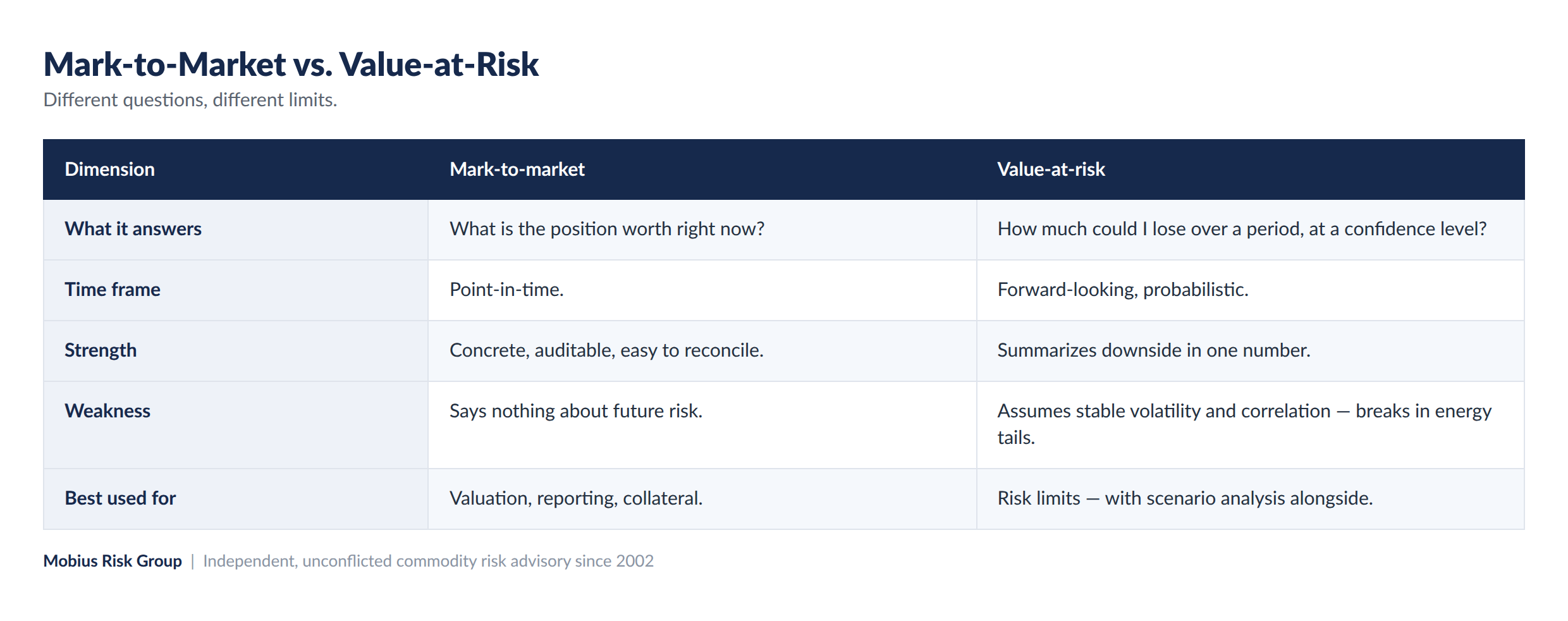

Mark-to-market tells you what a position is worth right now; value-at-risk estimates how much you could lose over a period at a given confidence level. Mark-to-market is concrete and auditable but backward-looking; VaR is forward-looking but relies on assumptions about volatility and correlation that break down in volatile energy markets. Serious programs use both, plus scenario analysis.

Measuring commodity risk means answering two different questions — what is this worth, and what could it cost me — with two different tools. Confusing them, or relying on one alone, is a common and expensive mistake.

What is mark-to-market?

Mark-to-market (MTM) values a position against current market prices, so it answers “what is this worth today?” It is concrete, auditable, and essential for reporting, collateral, and reconciliation — but it says nothing about what could happen next.

What is value-at-risk, and where does it fall short?

Value-at-risk (VaR) estimates the potential loss over a horizon at a confidence level. It is useful for setting risk limits, but it assumes volatility and correlation stay stable — an assumption energy markets routinely violate, especially in the tails where the biggest losses live. The comparison below lays out the trade-offs.

The practical answer is not to pick one but to use MTM for valuation and reporting, VaR for limits, and scenario analysis to cover what VaR misses.

Why does this matter more in energy?

Energy carries some of the highest implied volatilities in any market, and prices can gap on weather, storage, and geopolitics. That leptokurtic, fat-tailed behavior is exactly where constant-volatility models understate risk — so a measurement approach built for energy has to look beyond standard VaR.

How Mobius Risk Group approaches measurement

Mobius built M(β)risk™ to price market-based risk in a way that addresses the limitations of traditional VaR, alongside continuous mark-to-market in RiskNet™ — giving clients both the “what is it worth” and the “what could it cost” in one place. [confirm methodology detail]

Frequently Asked Questions

What is the difference between mark-to-market and value-at-risk?

Mark-to-market is the current value of a position; value-at-risk is an estimate of potential loss over a period at a confidence level. One is point-in-time; the other is forward-looking.

Why is VaR criticized for energy markets?

Because it typically assumes stable volatility and correlation, which energy markets violate. It can understate risk in the fat tails where the largest moves occur.

Should you use MTM or VaR?

Both, plus scenario analysis — MTM for valuation and reporting, VaR for limits, and scenarios for the tail risk VaR misses.

Subscribe to receive the latest Mobius Research & updates